This corporation tax tips for 2026 blog is for owner-directors of a company. It’s to make you aware of some of the tips and traps to avoid. All with the idea of saving tax and keeping on the right side of Revenue. These things are important, and it’s good to know about them to discuss with your advisors. The team here are very busy finalising 2025 accounts and corporation tax returns. These are a snapshot of some things I’ve seen in the first few months of this year

- Loans to Directors

- TRS on Medical insurance premiums

- Top up pension contributions

- Take a dividend

- Small benefit exemption

- Summary

Loans to Directors

There’s an Income Tax charge on loans to company directors. Pat and Sofie Barry owns 50% each of Barry for Hire Ltd. In 2024, Pat needed €40,000 to repair a property that he rents to sell it at the end of 2025. He’d repay the money to the company from the sales proceeds. As part of its corporation tax liability for 2024, the company paid Income Tax of €10,000. That year, it had a €150,000 profit from its trading activities. The corporation tax liability for 2024 was as follows

| Trading profit of €150,000 x 12.5% | €18,750 |

| Regross loan of (€40,000/8×10) x 20% | €10,000 |

| Total CT liability | €28,750 |

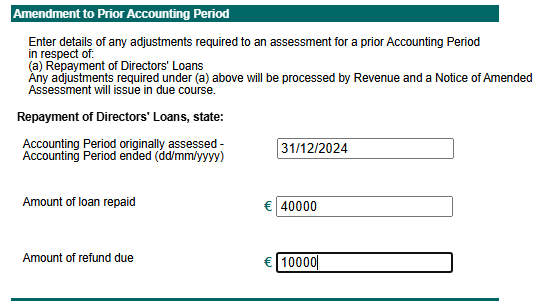

Not only is there an Income Tax charge, but there’s also a benefit-in-kind [BIK] for Pat. That’s at the rate of 13.5%, as it’s not for Pat’s private residence. If it was the rate would be 4%. Pat sold the property at the end of 2025 and repaid the loan to the company. We are now completing the CT return for 2025. In that return, we confirm to Revenue that the money was repaid. There are three entries in the return

CT return

In the 2025 CT return, you will include the following information

- The accounting period when he took the loan

- Value of the loan and

- The income tax on the loan

If you’ve good eyesight, unlike me, you’ll see from the picture that Revenue will act on this.

” Any adjustments will be processed by Revenue and a Notice of Amended Assessment will issue in due course”

This is an amended assessment for 2024 and will not impact the 2025 numbers. The 2024 amended assessment should show a final CT liability of €18,750. Revenue refunds the €10,000 Income Tax on the loan, so the amended liability for 2024 is the tax on the trading profit.

In practice, we did this, and nothing happened on the Revenue side. As in no amended assessment appeared in our ROS inbox. We sent a MyEnquiries to Revenue, and they sorted it then. Something to keep an eye on.

The key message is that the company must pay Income Tax on the loan. But the company can get a refund of that income tax once the company director repays the loan. There is a 4-year repayment period. If you don’t reclaim it within that time, Revenue will keep it.

TRS on Medical Insurance Premiums

TRS on medical insurance premiums is tax relief at source. The max is €200 for an adult, once the gross premium is €1,000 or more. For a child under 18, the max TRS is €100 once the premium is over €500. If the premium is less than €1,000 or €500, the TRS is 20% of the gross premium. Say it was €900 for an adult, then the TRS would be €180.

For 2025, Pat’s company paid the medical insurance for Pat, his wife Sofie, and their three children, Ben, Bob and Beau. The premiums were as follows

| Name | Premium | TRS |

| Pat | €1,200 | €200 |

| Sofie | €1,200 | €200 |

| Ben | €1,200 | €200 |

| Bob | €550 | €100 |

| Beau | €450 | €90 |

| Total | €4,600 | €790 |

For 2025, the company had a tax-adjusted trading profit of €175,000. Its corporation tax liability would look like this

| Trading Profit €175,000 x 12.5% | €21,875 |

| Add TRS on medical insurance premiums | €790 |

| Final CT liability | €22,665 |

The TRS is an entry on the 2025 Corporation Tax return Form CT1 for the company and is part of the final CT liability.

Claim a tax credit

We can claim a tax credit for the €790 that the company paid in Pat’s income tax return [Form 11] for 2025. Pat has paid BIK on the gross medical insurance premiums through his salary. If this hasn’t gone through payroll as a BIK, it should have. If it didn’t, then you would include the gross premium as a BIK in his tax return. The correct way is through payroll. By putting it through as a BIK in the tax return, Revenue lose out on the employer’s PRSI, but they’ll get the tax.

It’s a pretty convoluted way of doing things, but that’s the system.

Top-up pension contribution

The company could make a top-up pension contribution before the end of the year. When I say year, I mean the accounting year of the company, which is 31 December for Pat’s company. The company pays €1,500 a month into an executive pension scheme for Pat. At the end of 2025, we can see that the company has €250,000 in its bank account as we look after their bookkeeping. We contact Pat and confirm that he can put another €18,000 into his pension before the end of December 2025. He goes for it and transfers €18,000 to Aviva.

The company will get a deduction for both the monthly contributions and the top-up of €18,000 in 2025. The company pays €36,000 and gets a tax deduction for €36,000 in 2025. There is full tax relief once the top-up contribution is no more than the total of the ordinary annual contribution. There is no need to spread the top-up payment. Once it’s paid in 2025, it will get the tax relief in that year.

Take a dividend

This is where you take a dividend from your company to avoid the close company surcharge. Barry for Hire Ltd has a rental property. In 2024, there was a rental profit of €20,000. The Corporation tax rate is 25% on rental profits. To include the rental profit, the 2024 CT liability looks like this

| Trading profit €150,000 x 12.5% | €18,750 |

| Rental Profit €20,000 x 25% | €5,000 |

| Regross loan €40,000/8×10 x20% | €10,000 |

| Total CT liability | €33,750 |

After tax, there is €15,000 of rental profit that is available for the shareholders to take. There is a surcharge on companies that don’t distribute their investment income. This is known as the close company surcharge, and you calculate it as follows

| Rental Profit | €20,000 |

| Less tax on rental profit | €5,000 |

| Net rental profit | €15,000 |

| Deduction of 7.5% for a trading company | (€1,125) |

| Net distributable income | €13,875 |

| Surcharge 20% | €2,775 |

Pat and Sofie have two choices here. They either pay the surcharge or take a dividend to avoid paying it. If they decide to pay it, the liability falls into the CT return of the following year. As such, the company pays the 2024 surcharge as part of its 2025 CT liability

2025 CT liability with the surcharge

The 2025 CT liability with the surcharge for 2024 would look like this

| Trading profit of €175,000 x 12.5% | €21,875 |

| Add TRS on medical insurance | €790 |

| Add 2024 close company surcharge | €2,775 |

| Final CT liability | €25,440 |

To avoid paying the surcharge, they can take a dividend within 18 months of the year-end. The year-end is December 2024, so they have until the 30th of June 2026 to decide on the dividend or surcharge route. A dividend of €12,000 would avoid the surcharge in full.

| Net distributable income | €13,875 |

| Less dividends | (€12,000) |

| Balance | €1,875 |

Once the balance remaining after a dividend is equal to or less than €2,000, no surcharge applies. So, a dividend of €11,875 would also work to reduce the surcharge to nil. As they own the shares 50:50, they take a dividend of €6,000 each. They pay this in March 2026. The company must deduct 25% dividend withholding tax [DWT] and pay that to Revenue by the 14th of April 2026. That’s a DWT payment of €3,000 or €1,500 each. They both get a net payment of €4,500.

In 2026, Pat is on a salary of €45,000, and Sofie earns €28,000 from the company. They will pay tax on the gross dividend. That will increase Pat’s income to €51,000 for this year, and Sofie’s will increase to €34,000. As their combined income is less than €88,000 for 2026, they will only pay tax at the lower rate on the dividend. Plus, they’ll get a credit for the dividend withholding tax deducted and paid to Revenue.

Small benefit exemption

The small benefit exemption is a hot topic every year at Christmastime. It feels weird writing the word Christmas in March. From 1 January 2025, the benefit is up to €1,500 per employee and that’s for up to 5 vouchers. We’ve been harping on about this to clients for years. It’s great to see the voucher expense coming through in the accounts.

If there’s money in the company, this one is a no-brainer. Rather than wait to take a voucher at Christmas, Sofie decides to take it in March. She’s fed up of all the rain and gets busy booking the summer holiday. She buys two Ryanair vouchers for her and Pat for €1,000 each and uses them to pay for the flights to Tenerife in June. There might even be money left over for a few scratch cards on the plane! She told us about the vouchers when we met her in February, and we included them in her payroll ERR for February 2026.

This saves them €2,000, and they have met their reporting requirements. There is no employer’s PRSI, so the cost to the company is €2,000, and there’s no tax due by either director. They get the full spending power of €2,000.

Summary

The above is an example of some corporation tax tips for 2026, and there are lots more. We’ll do a follow-up blog, or part deux, later in the year. One of the advantages of doing bookkeeping for clients is that we see what’s happening during the year. That gives us information to help the clients where we see opportunities. Like the pension top-up or the small benefit exemption, if we don’t see it coming through.

It gives us a great overview of the client’s business and personal taxes. Lots of small tax tips add up over time. It keeps the companies and the clients as tax-efficient as possible and on the right side of Revenue, too. Otherwise, Mr Cody gets more of your money!

Do you and your company need help? If so, start here